Super for Housing

Home » Publications » Super for Housing

This paper discusses a proposal that home buyers be enabled to access their superannuation (hereafter, ‘super’) accounts when buying a home. Variations on this proposal have been suggested by the Treasury (1997), the Falinski Inquiry, the Bragg inquiry, the Federal Liberal and National parties (hereafter, ‘the Coalition’ ), and many others.

The paper is in three parts. The first discusses the rationale.

Building housing equity and superannuation are alternative methods of providing security in retirement. While the government has an interest in ensuring people make provision for their retirement, it does not have a clear interest in how they do so. If an individual wishes to save for their retirement by paying off a mortgage, instead of by accumulating superannuation, it is not clear why the government should obstruct that choice.

Owning a home is an important aspiration in Australian culture. Governments from different jurisdictions and different parties have enthusiastically encouraged it. That reflects a mix of perceived benefits to the buyer and to broader society. Allowing borrowers to use their superannuation would be a more efficient and equitable means of promoting home ownership than First Home Owners Grants; providing more assistance at lower fiscal cost, with less redistribution.

Furthermore, there are inefficient frictions and obstacles to access finance for housing, which superannuation may be able to reduce.

The second part of the paper discusses quantitative effects.

The median superannuation balance of first home buyers (including both balances of those who buy as a couple) is 92% of their deposit. So deposit-constrained buyers could almost double their demand for housing. Alternatively, 392,000 households may choose to buy a home earlier than otherwise, in which case the home ownership rate might increase by up to 4 percentage points, from 66% (in the 2019-20 Survey of Income and Housing) to 70%.

The third part of the paper discusses alternative approaches.

Superannuation could be accessed by withdrawing funds from the home buyer’s account. Many proposals and related schemes overseas (such as US 401(k)s or Canadian RRSPs) require that these funds be repaid, possibly with interest or — as the Coalition has proposed — as a share of capital appreciation when the property is sold. Under central assumptions, a typical borrower who used their super to pay for a deposit, then repaid it 10 years later upon sale of the property, would have a retirement account $53,600 lower at age 65.

The reduction in retirement accounts could be avoided if superannuation was used as security or collateral for home loans. This would overcome the deposit hurdle — the binding constraint for many first homebuyers — but would involve higher mortgage payments.

Both approaches achieve the objectives above. However, they also have a common limitation. They improve access to finance and hence boost the demand for housing. Unless the supply of housing increases, this will increase housing prices, aggravating housing affordability. For this reason, the Falinski and Bragg inquiries explicitly noted that any policies that make it easier to buy housing would need to be coupled with measures to increase supply. Specifically, the Falinski Report called for a relaxation of planning restrictions to allow greater housing density.

Moreover, further promotion of home-ownership is controversial, given the large subsidies and tax concessions that owner-occupiers already receive relative to renters. These problems (and the excess demand, noted above) would be mitigated if super for housing replaced existing subsidies, such as First Home Owners Grants.

Many supporters of using super for housing see it as a means of weakening compulsory superannuation. For them, the issues are clear and simple. However, this is a minority position. Compulsory super with a contribution rate rising to 12% is supported by all of Australia’s major political parties. That is important context for any discussion of changes to that system. Reform proposals need to address the system’s rationale.

Using superannuation for housing helps achieve the objectives of the superannuation system, while avoiding some of the disadvantages. Specifically, it facilitates saving for retirement, but allows the individual to choose how this is done, without creating an obstacle to homeownership.

There are several reasons the government makes people save for their retirement.

First is paternalism. There is strong evidence that people tend to be short-sighted — placing inadequate weight on the distant future (Hamilton, Liu, Miranda-Pinto, and Sainsbury, 2024). So they make inadequate provision for their retirement; a decision they later regret. Compulsory superannuation is intended to make a decision for people that society and their later selves will regard as in their own interest.

Second, superannuation partially replaces collective provision of retirement incomes with self-reliance. Society does not want retirees to be destitute, so provides an age pension at taxpayer expense. This can be thought of as providing insurance, and — like any insurance — it creates moral hazard. It reduces incentives to work and save. Compulsory self-provision has better incentives. The disincentive to work due to the age pension would be less if funds were going to the worker’s own retirement, instead of other people’s retirement. People will work harder for their own benefit than they will for others.

An overlapping but distinct argument is fiscal sustainability. Reductions in spending on the age pension would, in themselves, improve the federal budget balance; which, in turn, is desirable as it reduces the need for distortionary or confiscatory taxes. That benefit must be balanced against the distortionary implications of how one reduces the pension.

Against these objectives of compulsory superannuation, there are also costs. Compulsory superannuation distorts saving and investment decisions. It prevents individuals allocating income and investment over time and across assets in a way that suits their individual circumstances. In particular, it makes saving for a home deposit unnecessarily difficult. It requires people to borrow and save simultaneously, generating unnecessary financial intermediation and default risk.

Super for housing retains the benefits of compulsory saving, while reducing the costs. Retirement saving does not need to be in the form of superannuation; the savings could instead be in home equity.

Fiscal considerations are complicated. Superannuation reduces taxes on income when it is received and saved. Some see this as concessional. Others see it as moving to a more efficient expenditure base for taxation, offsetting other biases in the tax system. When compared to a (simple but distortionary) income tax benchmark, the tax concessions are regressive, favouring those on high marginal income tax rates. Super for housing arguably makes these problems worse. Housing is even more concessionally taxed and inequitably distributed than superannuation.[1] Nevertheless, those concessions seem to have community support. From an efficiency perspective, the concessional treatment of housing is an issue because it encourages too many resources to flow into that sector. However, this is more than offset by planning restrictions, which reduce supply overall. We discuss effects on housing demand and prices below.

A separate rationale for using superannuation for housing is that it facilitates home ownership at little cost to the taxpayer.

Owning a home is an important aspiration in Australian culture; and many want to assist and promote it. It is common to financially assist family members to purchase a home. This partly reflects a desire to help the next generation at an important but difficult stage in their lives. More broadly, governments from different jurisdictions and different parties have enthusiastically encouraged home purchase, for example through first homeowner grants and exemptions from stamp duty.

Whether they should do so is controversial. Home ownership has external benefits. Owners tend to have more civic engagement, they better maintain their garden, they contribute to local public goods and so on. Providing residents a ‘stake’ in their community promotes citizenship. However, these external benefits are estimated to be relatively modest (Glaeser and Shapiro, 2003). Homeowners also vote more conservatively than renters, though views presumably differ on the desirability and importance of that.

Home ownership is already heavily subsidised, relative to renting. This includes the exemption of imputed rent from income tax, exemption from land tax, full exemption from capital gains tax, and partial exemption from the means test for the age pension. First home buyers get further grants and tax exemptions. APRA imposes higher capital requirements on loans for rental property than on owner occupiers, creating a 20 basis point interest differential. Tax deductions for rental costs and subsidies to renters through Commonwealth Rental Assistance and public housing provide small partial offsets.

These subsidies and concessions to home ownership are paid for by those who do not own a home; that is, renters. Given that renters have less wealth and income than home owners, this seems inequitable.

The preferential treatment of owner-occupiers may reflect political distortions. The benefits are visible, direct and popular, while the costs imposed on renters are hidden and indirect. Claimed policy rationales are weak. Many externalities of home ownership, such as community participation, are more accurately described as benefits of long tenure. While long tenure for homeowners is encouraged by stamp duty (a tax on turnover), a more cost-effective approach would provide greater security of tenure for rental tenants; for example, by reducing the progressivity of land tax. It is sometimes suggested that APRA’s penalisation of rental property reflects its greater systemic risk. However, the absence of evidence supporting those claims (with lower gearing and arrears rates for investors[2]) suggest that political factors are more important.

To avoid exacerbating the preferential treatment for owner-occupiers and their consequent distortions, super for housing could replace less-justifiable subsidies, such as First Home Owners Grants. Whereas most First Home Owners Grants are about $10,000 per purchase, the median first home owner’s superannuation balance, discussed below, is $62,500. So super for housing could provide more assistance (measured in terms of initial cash outlay, not present value) at less fiscal cost.

Because First Home Owners Grants involve a subsidy from the taxpayer, they are distortionary and arguably inequitable. Consequently, the program is tightly restricted — for example, the limit on home value is $750,000 (which excludes most of Sydney). In contrast, if the buyer is borrowing from themselves, distortions are fewer, inequitable transfers are avoided and there is less reason for these restrictions. Changing First Home Owners Grants would require coordination with the states.

Accessing superannuation also overcomes some barriers to finance. Simultaneously saving via super while borrowing via a mortgage involves extra financial intermediation. The spread between borrowing and lending rates suggests this intermediation is costly, reflecting real resource costs and frictions like moral hazard and adverse selection (Quiggin, 1993). The financial system often seems to prevent worthwhile loans. For example, borrowers can be assessed as unable to service a loan even though the repayments are lower than the rent a tenant has reliably been paying. A difficulty in addressing these objectives is that the underlying market or regulatory failure is not clear, making the argument difficult to assess and appropriate remedies difficult to design.

Using super for housing would have widespread effects on many variables. However, quantification of these effects is lacking. Submissions to the Bragg inquiry on super for housing were riddled with claims lacking quantitative evidence. Most of the predicted effects were speculative. Many are difficult to take seriously.

This part of the paper attempts to partially remedy this. It does not provide a comprehensive assessment, but it is a start. We focus on how homebuyers might respond to the ability to access their super. This includes:

a) They could buy larger, nicer homes.

b) They could buy better located homes, closer to the city centre.

c) They could change the timing of home purchase, to buy earlier.

d) They could increase their deposit, reducing their mortgage.

e) They could buy instead of a lifetime of renting.

f) They could do nothing.

Section 5 helps to quantify options a) and b). Section 7 helps to quantify option c). Section 8 briefly discusses other effects, which may be less important.

For some purposes, how home buyers respond may not matter. If the objective is to give home buyers greater choice of how their savings are invested or when they buy, or more broadly to improve their welfare, then they might choose what is in their own best interest.

However, the implications for the housing market will differ. If the buyer chooses a larger or better-located home, the demand for housing will increase; that is, buyers wish to spend more. As mentioned in the introduction, unless supply is responsive, this would increase house prices, making housing less affordable for others.

However, if the buyer chooses to own their home instead of renting, it is not clear whether — or in which direction — the demand for housing would change. Buying a home to occupy involves vacating another dwelling. Because the mortgage payments on a dwelling usually exceed what it would rent for, liquidity-constrained households may buy a less-expensive dwelling than they previously rented. So some home purchases would involve a move to a less-expensive property and a reduction in the demand for housing. It is not clear that prices would be affected much, or even in which direction.

By how much could superannuation increase deposits?

According to the Survey of Income and Housing, the median deposit paid by first home buying households in the three years up to 2019-20 was $68,200, while their median superannuation balance was $62,500 (in 2022-23 prices, rounded). That is, the median first home buyer could increase their deposit by 92% if they were able to access their superannuation. Or they could reduce their own cash contribution by 92%, to $5,700. Obviously, if withdrawals are limited — as proposed by the Coalition — effects would be commensurately smaller.

These superannuation balances are high relative to other estimates. The Bragg Report (2024 p 37) echoed estimates by the CIS (2024) that superannuation balances of typical first home buyers were around $30,000 to $40,000. The new estimates use better data, which directly identify first home buyers. More importantly, we combine the balances of partners buying as a couple, which seems the relevant approach for financing a deposit. 71% of first home purchases are by couples.

The estimates can also be compared with the PBO (2022 p E-41) estimate that allowing withdrawals of super for housing would involve withdrawals of $21,325. That is on an individual, not household, basis and refers to a Coalition proposal which limited withdrawals to a maximum of 40% of the account or $50,000.

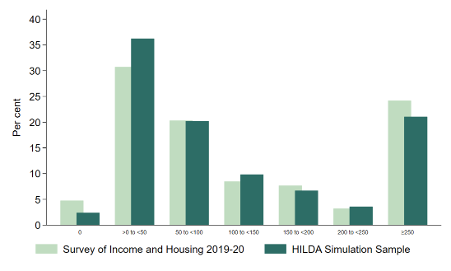

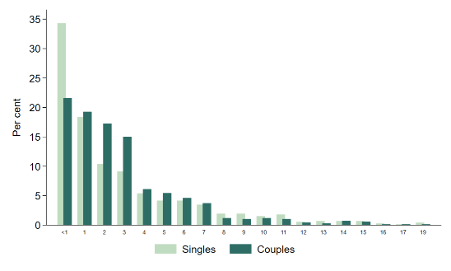

Chart 1 shows the distribution of superannuation balances as a percentage of housing deposits for households buying their first home. The light bars are from the Survey of Income and Housing (SIH) for 2019-20. The dark bars are from the Household, Income and Labour Dynamics in Australia (HILDA) survey using a sample we discuss below.

The two data sources show similar patterns. The following section discusses the data and reasons for the (small) differences.

Chart 1: Distribution of super balance as % of deposit

According to the SIH, 45% of first home buyer households have superannuation balances larger than their deposits. That is, were they able to access their super, they would not need to provide any up-front payment (other than to cover stamp duty, conveyancing and other administrative charges).

An implication of high super balances is that allowing full access to superannuation would involve a large increase in housing demand for those first home buyers who are constrained by a deposit requirement. This is discussed further below.

The Coalition has proposed limiting superannuation withdrawals to $50,000 a participant. This would substantially limit the impact of the policy. In today’s prices, 30% of single first home buyers have superannuation balances of more than $50,000 and 35% of couples have balances of more than $100,000. However, it is not clear why this limit should be applied. If the policy is desirable, this just reduces the benefits. The recent parliamentary inquiry chaired by Senator Andrew Bragg did not recommend limits.

At the other end of the scale, 35% of first home buyers have super balances less than half as large as their deposit. For these buyers the ability to access their super is of relatively limited benefit.

In the middle, the remaining 20% of first home buyers have super balances between 50 and 100% of their deposit. For these buyers, accessing their super would be of substantial help, though it would not obviate the need for a large cash contribution from the buyer.

The SIH surveyed 15,011 households in 2019-20, of which 1,624 bought a home within the past three years which was the first home for 565 households. That translates into a national average of 140,000 first home purchases a year. The SIH asks about deposits at the time of purchase, and home equity at the time of the survey. We use the former.[3]

The HILDA estimates require more of an explanation. HILDA has surveyed the same respondents each year from 2001, with detailed questions about finance every four years. We define a first home buyer as a respondent who says they live in a dwelling they own, excluding those who said this in previous surveys or the first survey. We pool the surveys from 2002 to 2022, update to 2022-23 prices and date purchase from the response to the question “In what year did the household purchase … your current home?” Superannuation balances are interpolated between financial waves assuming constant compound growth rates.

The longitudinal nature of HILDA enables us to estimate a history of superannuation balances for first home buyers, which we use in simulations below. This involves restricting the sample to first home buyers who, at a minimum, record a superannuation balance in the financial wave immediately before and after purchase. One effect of this restriction is to eliminate buyers who purchased as a couple but were not cohabiting in the preceding wave. Our sample is 1,398 purchases by 2,073 individuals, comprising 723 singles and 675 couples. This is a much smaller proportion of couples than the SIH and we reweight our results to adjust for this.

While the two estimates shown in Chart 1 follow similar contours, super/deposit ratios are somewhat higher in the SIH (median 94%) than in HILDA (median 76%). This largely reflects lower deposits in the SIH (median $68,400) than in HILDA (median $76,900). We are not able to explain the difference, though expect the SIH to be more representative.[4]

Later sections discuss features of the data that bear upon later results. Appendix I discusses the HILDA sample used in simulations.

To estimate the effect on retirement accounts, we make some simple but representative assumptions. Consider a policy in which home buyers are able to withdraw from their superannuation account and are required to repay that amount with a proportionate share of capital appreciation on sale of the home. This is a simple version of the Coalition’s policy, without restrictions.

Suppose a borrower withdraws the median (for first home buying households) superannuation balance of $62,500. According to the SIH, the median time spent in a dwelling by owner-occupiers is 10 years (Bloxham, McGregor and Rankin 2010, Graph 3). So assume the loan is repaid to the superannuation fund after 10 years.

The average long-term real return on superannuation funds in the accumulation phase, after taxes and investment fees, has been about 4.5% per year.[5] So one might expect the superannuation account to forgo that return, reducing the balance by $97,000 after 10 years. All these estimates are in constant 2022-23 dollars and assume no change in super contributions.

Partially offsetting this, the loan would be repaid with a share of the capital gains in the house. The average real rate of capital appreciation on Australian housing since 1955 has been 2.4% a year. (Stapledon, 2012). So the initial ‘equity share’ of $62,500 might be expected to grow to $79,200.

Subtracting capital appreciation ($79,200) from typical superannuation returns ($97,000), the superannuation account would be $17,800 smaller immediately after repayment. Suppose the borrower works for a further 25 years — for example, if they bought at age 30, sold and moved house at age 40 and retired at age 65. Holding other things equal, the lower balance would accumulate to $53,600 (in 2022-23 dollars) at retirement. For comparison, the median superannuation balance of 60-64 year-olds is $183,524 (Taxation Statistics 2020-21), though this will rise as past increases in contribution rates flow through.

Another illustrative alternative is to assume that, instead of the withdrawal being repaid, it is retained until retirement, when the rest of their super balance is withdrawn. Extending the period of the loan from 10 to 35 years, and excluding repayment, the superannuation fund would be $291,600 lower at retirement age. This scenario would apply if withdrawals could be rolled over to later home purchases as recommended by the Bragg inquiry. Roll-over capability prevents home owners being locked in a dwelling that no longer suits their needs. However, it would involve a large reduction in retirement accounts.

In principle, large withdrawals like this would also occur when withdrawals are limited to first home buyers and the buyer remains in the property until retirement. In practice, that is rare. Only 25% of home buyers remain in the one property for at least 20 years and only 5% for at least 40 years (Bloxham, McGregor and Rankin 2010, Graph 3).

The estimated reduction in retirement accounts will be offset by increased home equity. The simplest case is to assume that the accessed superannuation was used to increase the deposit and lower the mortgage, at a real rate averaging 3%, on an otherwise unchanged purchase held for 35 years. The increased home equity would accumulate to $175,800. That compares with the reduction in super balance of $291,600. The difference reflects the higher average returns on super than on mortgage repayments.

A more comprehensive comparison would also factor in savings in lenders mortgage insurance, increased equity from deposit-constrained buyers purchasing more expensive housing, and from wider home-ownership. Even allowing for these, the borrower is likely to be financially worse off, as the foregone returns from superannuation exceed those from paying off a mortgage. Nevertheless, borrowers will choose to access super (as discussed in section 9) for several reasons. Although super returns are high on average, they are also more variable and uncertain. Risk-averse borrowers will prefer the certainty of lower mortgage payments. Non-financial benefits of home ownership, like security of tenure and freedom to renovate, provide further compensation. Because many of those who access super for housing are likely to be financially worse off, but better off in non-financial terms, assessing the distributional and equity implications of the policy is difficult.

Contrary to common suggestions, the more comprehensive comparison discussed above should not include means testing of the age pension. Superannuation accounts are included in the age pension assets test but most home equity is not. However, transferring wealth from retirement accounts to home equity prior to retirement, need not affect the assets test after retirement. Retirees who wish to avoid the assets test can withdraw their super as a lump sum and reduce their mortgage. Conversely, retirees with high housing equity and low cash flow can take reverse mortgages (Moneysmart, 2025). The composition of pre-retirement assets does not greatly constrain post-retirement portfolios.

Assessing that net financial returns from superannuation exceed those from paying off a mortgage is standard. An exception is Rice and Ng (2024, Submission No 40) who are cited positively by the Bragg Report (2024 p 9). Rice and Ng assume superannuation returns of only 5% nominal (presumably 2.5% real). This assumption is well below the estimates in endnote 5 or longer-term estimates of equity returns (Mathews, 2019). It is possible that super returns will be lower in future, but in that eventuality, mortgage rates might also be expected to be lower.

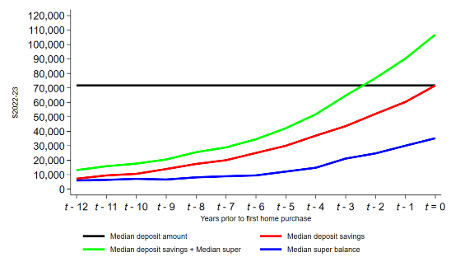

Were home-buyers able to access their super, one option is to buy the same housing but purchase earlier. Chart 2 illustrates how this can be quantified. The sample is HILDA respondents who purchase their first home as a single and for whom we have a history of superannuation balances.

Chart 2: The home buying decision for single home buyers

The median deposit for this sample is $72,000, shown as the black horizontal line. (All estimates in this section are from HILDA, in 2022-23 dollars, using the Consumer Price Index, rounded to the nearest $000).

The median superannuation balance of single home buyers, when they buy their first home, is $35,000, lower than the median balance of $60,000 for all first home buyers, represented in Chart 1. Super balances up to this point are shown as the blue line. As expected, they increase steadily with time, reflecting contributions and investment returns. The left-most point on the blue line represents the median super balance for first home buyers for whom we have super data at least 12 years prior to purchase. The right-most point is the super balance in the year of purchase, for which we have a larger sample. The increase in sample size also involves a slight change in the composition, increasing the slope of the line relative to a fixed sample.

Data on how buyers fund their deposits are poor. The red line in the chart assumes they gradually save the full deposit at constant rate from when they enter the workforce until they buy. For an individual borrower, this would be a straight line. However, the compositional change mentioned in the previous paragraph imparts a slight non-linearity. Those who buy when young have saved faster than those who buy when old. A constant saving rate is a strong simplifying assumption. We discuss these issues (including parental transfers) in Appendix II.

Were superannuation able to be accessed, buyers could use the sum of the red and blue lines as a deposit, shown as the green line. As shown in the chart, this reaches the deposit almost three years earlier than the actual purchase date; implying the median single home buyer could own their home by 27 years of age instead of 30 if they had access to their super.

We say could, not would. We are measuring financial capability, not behaviour. This is an upper bound on the actual response. Section 9 discusses the extent to which buyers take up these opportunities.

The financial position of a single home buyer is simple, but it is not typical. The substantial majority of first home purchases — 71% according to the SIH — are by couples. Couples are, on average, 2 to 3 years older than singles when they purchase their first home. Reflecting that, and higher combined income and demographic differences, they have substantially higher combined superannuation balances at the time of purchase:- $94,000 compared with $35,000 for singles. It is the combined balances of the couple that would determine the amount of super available for the deposit. Somewhat surprisingly, the deposits paid by couples are only slightly larger than singles. The median deposit of a couple purchasing their first home is $81,000, compared to $72,000 for singles. As a result, couples can bring forward their purchase by more than singles.

A limitation of our longitudinal data is that couple respondents often represent survey respondents partnering with people from outside the survey, for whom we do not have a history of superannuation balances. So a version of chart 2 for couples would largely reflect changes in the composition of our sample. More importantly, couples will enter HILDA only after they share a household. Outside partners with large superannuation balances before this — and hence the capacity to buy earlier — will be excluded from our estimates. This imparts a downward bias to our estimates of homeownership. However, as the ‘couple’ were not cohabiting it is not clear they would have had both the intent and ability to jointly purchase, so the truncation may not be severe. Appendix I further discusses this complication.

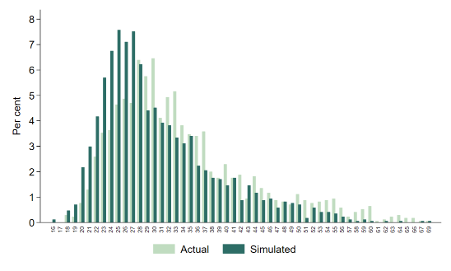

We can construct estimates corresponding to Chart 2 for each of the 1,398 first home buyers in HILDA for whom we have their actual deposit and history of superannuation balances. Chart 3 shows the distribution by age of first home buyers in the simulation sample (the light bars) and when they may have bought were they able to access their super (the dark bars).

Chart 3: Age at purchase of first home; Potential effect of access to superannuation

Chart 4 shows the difference between these distributions; that is, how much earlier each of these respondents could have bought. The average bring-forward is 2.8 years.

Chart 4: Potential bring-forward of home purchases

These estimates represent a temporary increase in the flow into home-ownership and, assuming no change in the exit flow, a permanent increase in the stock. To calculate the increase in home-ownership from people being able to buy earlier, we multiply the average bring-forward (2.8 years) by the annual flow of first home buyers in the SIH (140,000), giving 392,000 new homeowners. That would represent an increase in the home ownership rate of 4% of households, from 66% (in the 2019-20 SIH) to 70%.

The analysis of the Parliamentary Budget Office (2024) assumes, as they were asked to, that 20% of renters (or approximately 6% of households) would purchase a home in response to the Coalition’s proposal. That would be similar to this paper’s estimates if one assumed that all home buyers used their superannuation to buy earlier and almost all the available super was accessed (not 40% as per Coalition policy). The PBO assumption would be higher than our estimates if some first home buyers were to instead use their super to buy more expensive homes.

As noted in Section 4, there are many different ways in which home buyers might respond to the ability to access their super. Sections 5, 6 and 7 discussed some of the more important of these. Two other possibilities are worth noting.

Home buyers might respond to the ability to access their super by increasing their deposit, reducing their mortgage. This seems unlikely to be important. It effectively means withdrawing funds from a high-return asset so as to reduce a mortgage rate with a lower return. As discussed in section 7, this would reduce the lifetime income of a permanent home-owner, who rolls over their superannuation liability, by $115,800 (=$291,600–$175,800). Unless a borrower is paying prohibitive lenders mortgage insurance, accessing superannuation is only financially beneficial for constrained borrowers unable to buy as much or as early as they would like.

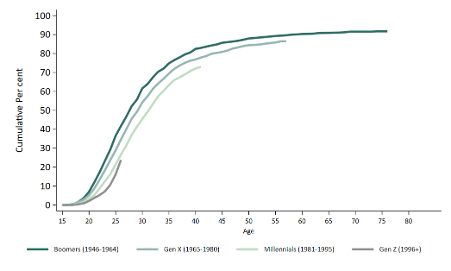

Another possibility is buying instead of a lifetime of renting. This is difficult to quantify, though it is possibly also unimportant. Retirees already have access to their superannuation for any purpose, including buying a dwelling with a lump sum. However, very few retirees take advantage of this opportunity. The rate of current-home-ownership plateaus at about 80% by the age of 60. As shown in Chart 5, the rate of ever-having-owned plateaus at about 90% at a similar age. 96% of transitions into home-ownership observed among those currently in their 60s and 70s (the Baby Boomers) occurred prior to their 50th birthday. The policy of ‘super for housing’ is sometimes motivated by a desire to increase security in retirement and opposed by those who fear it makes retirees ‘asset rich and cash poor’. However, the policy does not substantially change the incentives or constraints facing retirees.

Chart 5: Cumulative percentage of transition into ownership of residential property from age 15 by generation, 2022

Notes: Estimates are one minus the estimated survival probability of being yet to purchase a residential property using the method of Kaplan & Meier (1958). Weighted estimates using the responding person sample weights.

Source: Household, Income and Labour Dynamics in Australia survey wave 22.

However, while the effect on lifetime ownership may be small, it is presumably positive. So the effect of allowing super for housing on home-ownership is presumably slightly larger than our estimates. Quantification of this is for future research.

The previous sections suggested that allowing access to super would enable first home buyers to offer up to $62,500 (at the median) more for their home deposits; increase the home ownership rate by up to 4 percentage points; or some combination of these.

These are upper limits, assuming that buyers use their entire superannuation balances. How much of these available funds would they actually access?

As Deloitte (2024) and the Super Members Council (SMC) (2024) suggest, New Zealand’s KiwiSaver program provides a guide.[6] KiwiSaver provides defined-contribution, tax-preferred retirement accounts from which members can withdraw to purchase a first home. Withdrawals for first home purchase have averaged 40,400 a year over the past five years (NZ Inland Revenue, 2024). Total loans to first home borrowers have averaged 28,100 a year (RBNZ, 2024). Assuming that 71% of these loans are to couples, as in Australia, that would put the number of individual first home buyers at about 48,100 a year.

This suggests that 40,400/48,100 = 84% of first home buyers withdraw from their KiwiSaver accounts to buy a home. This is marginally less than the 87% estimate of Deloitte and SMC, reflecting use of more recent data than they had available.

The average withdrawal for first home purchase in 2023-24 was NZD$37,100 ($33,500 AUD), which is slightly larger than the average KiwiSaver account balance of NZ$33,100. That suggests withdrawals come from larger than average accounts and that most withdrawals are close to the full account balance.

Perhaps the main difference between KiwiSaver and Australian superannuation accounts is that the latter are compulsory and so include funds the contributors would not have voluntarily made. Accordingly, more superannuation funds might be expected to be withdrawn when given the opportunity. That is, the take-up from super might be higher.

Other sources of information do not provide as precise a guide and are somewhat mixed. However, on balance, they also point to a high take-up rate.

25-34-year-olds in Sydney and Perth tell Troy and coauthors (2023) they are anxious to buy, but the deposit is a major barrier. In our discussions with finance and housing industry participants, we hear similar reports. However, the deposit constraint becomes less binding as mortgage rates rise.

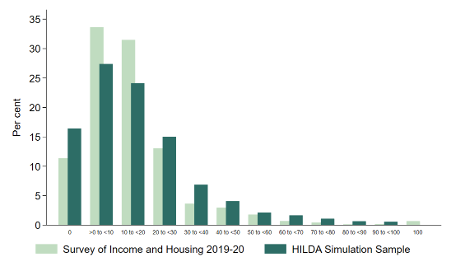

Chart 6 shows the distribution of deposits, as a proportion of purchase price. In the SIH, 76% of first home buyers’ deposits are less than 20% of the purchase price, with 45% being less than 10% of the price. These borrowers will tend to be short on liquidity. Many will be paying Lenders Mortgage Insurance. Current market quotes suggest that Lenders Mortgage Insurance is about 1% with a 15% deposit, 2% with 10% or 4% with a 5% deposit. The potential ability to reduce mortgage insurance is a substantial financial advantage of accessing superannuation, especially for households with little wealth. In contrast, only 10% of first home buyers make deposits of 20% or more and only 7% make deposits of 30% or more; these borrowers would have little need to access superannuation.

Chart 6: Distribution of deposits as % of purchase price

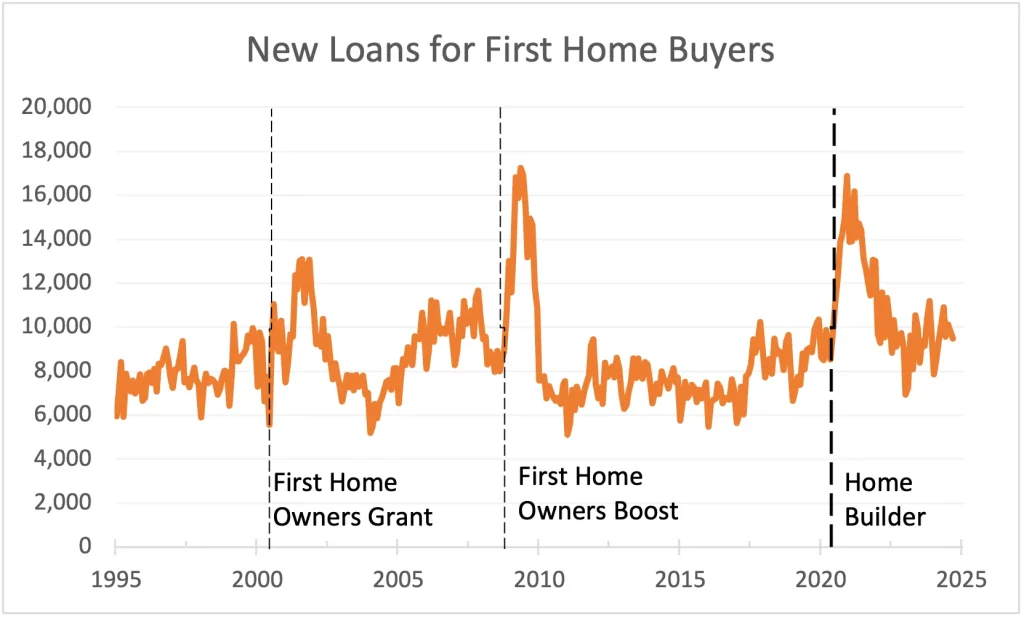

First homeowners react quickly and strongly to new finance. As shown in Chart 7, loans to owner-occupier first homeowners soared after the First Home Owners Grant of $7,000 in July 2000 (doubled in March 2001), the First Home Owners Boost of up to $14,000 in October 2008 and again after the HomeBuilder grants of up to $25,000 in June 2020.

Chart 7: New Loans for First Home Buyers

Source: ABS Lending Indicators, spliced with Housing Finance prior to 2002.

This experience suggests that first home buying might also surge in response to availability of funds from superannuation. However, there are important differences. First home buyer grants have been substantially smaller than superannuation balances. These grants raised lifetime income, whereas accessing superannuation does not — and may even reduce it. Increased grants were accompanied by other measures that boosted lending, in particular large reductions in mortgage rates (though these had smaller effects on other borrowers). And some of the response reflected changes in the timing of loans that would have occurred anyway.

During the pandemic, people were allowed to withdraw up to $20,000 from their superannuation accounts. Approximately one sixth of the population did so, most withdrawing the maximum amount, using the money primarily for gambling and consumer non-durables. Hamilton, Liu, Miranda-Pinto, and Sainsbury (2024) conclude that a large share of the population seemed to place remarkably little weight on the need to save for their retirement. However, the pandemic withdrawals were rarely used for housing; so while this episode indicates tightly-binding liquidity constraints, it is less informative about the precise consequences of relaxing those constraints.

In the United States, 401(k) schemes are defined-contribution tax-preferred retirement accounts, from which participants can borrow without penalty, subject to some conditions. Between 2016 and 2020, 29% of 401(k) participants borrowed from their account. However, only 2% of loans to participants (by amount outstanding) were home mortgages (Holden, Bass, and Copeland, 2023, endnote 20).

Since the 2022 election, the Coalition parties have advocated a Super Home Buyer Scheme. This was modelled on a scheme proposed by Tim Wilson, the then member for Goldstein. It would allow first home buyers to withdraw up to $50,000 or up to 40% of their superannuation (whichever is less) to invest in their first home. The invested amount would be returned to their superannuation fund when the house is sold, including a share of any capital gain.

Although this proposal is often described as ‘withdrawing’ from superannuation, the funds need to be repaid if and when the property is sold; so it is more accurately described as a loan — or perhaps more precisely as an equity investment, given that the repayment would comprise a share of any capital gain.

As discussed in previous sections, this policy would reduce retirement account balances, offset by higher home equity. It would increase the demand for housing, which would increase housing prices unless offset by other measures to reduce demand or increase supply. The limits of 40% and $50,000 per withdrawal would each place about a third of first home buyers’ superannuation accounts off limits (with substantial overlap).

Withdrawal of superannuation funds that are not repaid raises tax issues, given that initial contributions are concessionally taxed, relative to an income tax benchmark. From an efficiency perspective, allocation of extra resources to housing arguably acts as a partial offset to the bigger distortion created by zoning restrictions. In a free market we would have a physically larger housing stock (worth less, because demand is price-inelastic). Equity implications are unclear. Many commentators argue that the preferential taxation of owner-occupied housing (discussed in Section 3) is unfair, and that super for housing would exacerbate this unfairness. However, this appears to be a minority view given the “strong consensus” (Treasury, 2015, p67) against taxing income from owner-occupied housing. Tax concessions for owner-occupied housing are enormous (when measured against an income tax benchmark) and super for housing would not materially change that.

The Coalition’s plan would reduce superannuation balances. Among some of the plan’s supporters, a diminution of the role of compulsory superannuation is a major advantage. However, the plan’s designers seem to have seen this as a complication, if not a problem – presumably this is why loans are limited to 40% of the balance or $50,000.

The reduction in retirement saving could be reduced if the loan had a higher interest rate. For example, in the United States, individuals can borrow from their retirement fund, called a 401(k). Loans typically have a short repayment period and an interest rate tied to a benchmark like the prime rate, currently around 10% a year. A loan like that makes paying the deposit easier but subsequent loan repayments are harder.

The Coalition’s proposed Super Home Buyer Scheme resembles the Government’s Help to Buy Scheme in important respects. Both provide assistance with the deposit, repayable as a share of the capital gain. The fundamental difference is that under the Coalition’s scheme, the buyer is borrowing from their own superannuation, whereas under the Government’s scheme they borrow, at a concessional rate, from the taxpayer. Under the Coalition’s scheme, the buyer forgoes the earnings they would otherwise receive on their superannuation, whereas the Government’s scheme is a subsidy.[7] Flowing from this, the Coalition scheme offers a moderate amount of assistance to a large number of home buyers, whereas the Government scheme provides large assistance to few buyers. Whereas about 140,000 first home buyers a year would be eligible for the Coalition proposal, the Government’s proposal is restricted (via income and property value thresholds) to 40,000 borrowers. The Coalition is offering up to 40% of the superannuation balance, which might be $25,000 for the median first home buyer. The Government is offering much larger sums — up to 40 per cent of the value of new homes and 30% for existing homes. That represents about $255,000 for new and $172,000 for existing, based on mean self-reported values by first home buyers in the 2019-20 SIH.

An alternative approach is to allow superannuation to be used as collateral or security for housing loans. This was proposed by Tulip (2020) and the Falinski (2022) and Bragg (2024) Reports.

The idea is that deposits would decline by the full amount of the superannuation balance (or possibly more, if growth in the balance is expected). The size of the loan, and hence repayments, would increase commensurately. Superannuation balances would only be reduced in the infrequent and unexpected event of loan foreclosure. Legislation governing superannuation would need to be amended.

According to Jarden, 5% of new home loans have a parental guarantor. This policy would enable borrowers without wealthy parents to use their own superannuation fund as guarantor. A more ambitious variation would also enable parents to use their superannuation as security for their children’s loans.

Foreclosures are infrequent. Bergmann (2020) examined 2.8 million residential mortgages that were reported in the RBA’s Securitisation Dataset at any point between July 2015 and June 2019. Around 45,000 of these loans entered 90+ day arrears at some point during this period (around 1.5% of loans) and only 3,000 loans (0.1%) proceeded to foreclosure. There are reasons for suspecting this foreclosure rate to be unusually low. In particular, the period was short and saw rising house prices, though it also saw an increase in unemployment. However, NSW Courts data on mortgage repossessions from 2014 to 2024 are similarly tiny (Rachwani and Barrett, 2024). Even if foreclosures were an order of magnitude greater, they might still be considered infrequent.

Because balances are unlikely to be touched, there is no clear reason for limiting the scheme. That applies both to limits on the proportion of the balance or to limits on eligible recipients. The Falinski and Bragg Reports recommended that use as collateral be limited to first home-owners, but the reason for this is not apparent.

Using superannuation as collateral has much in common with the previous policy of borrowing from superannuation, including the underlying rationale. In political terms, both policies transform superannuation from an obstacle to home ownership into a vehicle towards it. However, there are also differences, as summarised in the following table. For simplicity, it is assumed that buyers respond only by changing their deposit — the timing and value of the purchase are unchanged.

Table 1: Policy Comparisons

Preferences between the two policies partly depend on how one weights the different rows. If protecting superannuation balances was most important (due to either economic considerations or political constraints), or if one thought the deposit was the biggest hurdle to home ownership, collateral would be preferred. Alternatively, if one thought the biggest obstacle to ownership was high mortgage payments, withdrawing from superannuation and repaying with capital gains would be more effective. However, policy-makers need not choose between these alternatives; that decision could be left for the borrower.

We estimate that a policy of super for housing would substantially increase the demand for housing and/or boost the homeownership rate. Presumably, a mix of the two. These effects might come at the expense of a reduction in retirement incomes, an effect that could be avoided by using superannuation as collateral.

For reasons of simplicity and brevity our estimates focus on some simple and direct effects and are not comprehensive. This paper indicates that responses to accessing super might be substantial, but it does not estimate the relative importance of different responses. Nor does it examine how subsequent homeownership and saving behaviour might change after a dwelling is purchased. Further research will provide a fuller picture.

This appendix details the approach taken to form a sample of first home buyers for the simulation in Section 7.

The 21 HILDA surveys that took place between 2002 and 2022 (inclusive) include data on some 33,190 responding persons. Of these, 15,700 never owned, 12,411 were home-owners when they entered the study and 5,079 became owners between 2002 and 2022 (shares that differ from those reported elsewhere as they are for individuals, not households). HILDA includes data on various types of wealth every four years beginning in 2002. Of the new home-owners, 3,276 responded to these ‘wealth waves’ either side of their home purchase, from which superannuation balances at the time of purchase can be inferred.

For singles, (which includes couples who cohabit but do not buy jointly) estimating super balances at the time of home purchase is straightforward. For couples, we want super balances for both members from the wealth waves immediately before and after the purchase, which involves excluding couples who buy jointly but were not cohabitating (and hence both surveyed) in the wealth wave immediately prior to the home purchase. This is an issue for the representativeness of our sample. It leaves 2,732 responding persons.

We only have superannuation histories of couples from the first wave after which they start sharing a household and hence when both partners enter the survey. Our bring-forward estimates are truncated at this point. Many couples may have been able to purchase earlier, but we do not have a full record of their super prior to cohabitation.

Excluding further missing observations and respondents whose transition into first homeownership is other than by buying (for example, by partnering with a homeowner who chooses to confer upon them equity in the dwelling) leaves 2,073 individuals, comprising 723 singles and 1,350 members of couples. That represents 1,398 households or purchases.

A difficulty in estimating how much earlier people might buy a home, given greater access to finance, is the scarcity of information on how first home buyers obtain their deposit. HILDA measures wealth in the years before and after home purchase. Unfortunately, ownership of many assets, including investment property and equities, is jointly attributed to the household, not the individual. (Ownership of owner-occupied property, superannuation and individual bank accounts are attributed to the individual). In many cases, assets classified as collectively owned will actually be owned by other members of the previous household a home buyer is moving from (for example, parents) and would not be available to the buyer. Of the 426 home purchasers who shared their household with other income units in the wealth wave prior to purchase, 232 shared the household with at least one parent.

A simpler approach to estimating the accumulation of home deposit saving is to assume that each individual’s savings grow at a constant rate from when they first begin paid work, to the deposit amount reported in the year they purchase. This is shown in the simulations in Charts 2, 3 and 4.

An alternative assumption is that savings grow at a constant percentage rate from an initial value of $1000 when they first begin paid work, to the deposit amount reported in the year they purchase. This assumption better describes buyers who step up their saving as purchase approaches or those for whom asset growth is due to compounding returns on investment. Under this assumption, the average bring-forward in purchase timing would be 2.1 years instead of 2.8 and the homeownership rate would increase by 3 percentage points.

Another uncertainty concerns parental assistance and bequests. Many first home buyers rely on the ‘bank of Mum and Dad’ for loans, gifts and guarantees. However it is unclear how this varies with time, buyer’s saving or other factors. At one extreme there will be those whose parents will cover the deposit at any time. These purchasers were never liquidity-constrained; so it seems unlikely that access to super would change the timing of their home purchase. On the other hand, there will be those whose parents or an inheritance provide most, but not all, of the deposit; so a small amount of super could have a substantial impact on the timing of the purchase.

Data on the importance of parental assistance are mixed and difficult to interpret. In a survey of 25-34 year olds, 43% of whom were homeowners, only 8% had received an inheritance, gift or loan from family members of $20,000 or more (Troy and co-authors, 2023, Figure 24). Many more received smaller transfers (most less than $5,000), which would have little effect on buying decisions. Parental support is important in many of Troy and co-authors’ case studies but their wider survey suggests these experiences are unrepresentative.

A 2023 survey of 282 mortgage brokers, by investment group Jarden, suggests a much larger role. 15% of all borrowers (implying most first home buyers, assuming they are most recipients) received help from their parents, with 10% receiving monetary gifts or loans and the remaining 5% receiving guarantees. Among those receiving monetary assistance, the average was $70,000. It is not clear why these estimates are so much larger than those of Troy and co-authors.

The web site Finder reports that more than 60% of first home buyers in Australia receive some form of financial assistance from their parents to buy their first home. The average assistance was $33,278. However, details of the survey are not provided and its representativeness is unclear.

Official surveys do not provide data on the value of contributions, however they are closer to the estimates of Troy and co-authors in indicating parental assistance is uncommon. The 2019-20 SIH indicates that 23% of first home buyers received assistance from non-government sources, most of whom are presumably parents. 15% of respondents to HILDA who bought their first home in Sydney, Melbourne or Perth in 2015-18 reported parental assistance, while in less expensive markets, the share was 8% (Pawson and co-authors 2023, Tables 7 and 8). These shares are double what they were in the early 2000s but still small.

Overall, most authoritative sources suggest that only a small minority of first home buyers seem to get parental assistance, the value of which may be small. The proportion is higher in expensive markets like Sydney. However, the much larger estimates from Jarden and Finder make estimates uncertain. There is even greater uncertainty about how parental support might affect the contribution from super.

Thanks to Matt Bowes, Simon Cowan, Matt Linden, Karla Pincott and participants at the Australasian Housing Researchers Conference for helpful comments.

This research report uses unit record data from the Household, Income and Labour Dynamics in Australia (HILDA) Survey. The HILDA Project was initiated and is funded by the Australian Government Department of Social Services (DSS) and is managed by the Melbourne Institute of Applied Economic and Social Research (Melbourne Institute). The findings and views reported in this paper, however, are those of the authors and should not be attributed to either DSS or the Melbourne Institute.

Matthew Taylor was Director of the Intergenerational Program at the Centre for Independent Studies while preparing this research report.

Peter Tulip is Chief Economist at the Centre for Independent Studies.

[1] Comparisons of “inequity” are sensitive to the measure; however one relevant gauge is that superannuation is much more widely held. 87% of adults aged 25 to 64 are covered by superannuation whereas only 65% own their home.

[2] The RBA (2023, Graph 3.8) estimates that, in the event of a 30% fall in property values from their January 2023 levels, about 50% of recent first homeowner-occupiers would have been in negative equity, compared to about 30% of recent loans to investors.

[3] Disconcertingly, the self-reported median equity of first home buyers in 2019-20 was $130,000, well above the $68,200 deposit they paid. In principle, the difference could reflect capital gains since purchase, however national house prices were relatively flat in the 3 years before the survey.

[4] Two factors account for a small part of the difference. First, we use the full history of HILDA from 2002. Purchases early in the sample will be by buyers who had relatively low compulsory superannuation contributions. Second is differences in timing. In the SIH home purchases are reported any time within the past three years, whereas superannuation balances are measured just prior to the survey date. So super in the SIH has had a year or two’s extra growth since many home purchases.

[5] Chant West (2025), a leading data collector, reports a 32-year average return for the median growth fund, after taxes and investment fees, of 8% nominal or 5.4% real. ASFA (2024) report a 30-year average net return of 7.3% nominal or 4.4% real, which presumably averages between higher returns in accumulation accounts (the relevant comparison) and lower returns in retirement accounts. The Retirement Income Review – Final Report (Table 6A-9, p515) assumes an average net return of 6% nominal and 3.5% real but notes this is conservative relative to historical returns.

[6] We are indebted to Matt Linden of SMC for discussions about these estimates.

[7] Under the Government scheme, the borrower foregoes capital gains on the government’s share, which have historically averaged 2.4% a year, while saving on mortgage payments of about 3% a year, both in real terms. The borrower would also pay for repairs and rates on the whole property,